If the insurance companies rethink their traditional roles and adopt an insurance ecosystems mindset, they will have enormous opportunities to create new sources of revenue. The insurance industry is on the verge of a paradigm shift due to an ongoing drive toward digitization. The pace of this change is increasing with the ubiquity of a large amount of electronic data, artificial intelligence, and growing mobile interfaces.

A platform refers to a business model that enables multiple participants (producers and consumers) to connect to it and interact with each other. A common platform helps them to create and exchange value. Many successful companies, like Facebook, are designed on the platform business model. However, an ecosystem refers to an interconnected set of services that enables users to fulfill various requirements in one integrated experience.

The rise of ecosystems and platforms: how insurers can get started?

Companies with an insurance ecosystems approach can scale at a much faster rate comparatively as this strategy has the ability to facilitate the expansion of insurers into completely new areas of business by using complementary methods. Insurance companies can provide innovative hybrid solutions and services while partnering with other industries. For example, smart parking, preventive care, and predictive maintenance. Insurers can also multiply their risk engineering capability by accessing insights based on sensor data from other industries.

Structuring and implementing an ecosystem strategy does not come easy as it requires sustained commitment and dedication. Companies aiming to start an ecosystem approach should focus on a couple of areas.

First, in the distribution economy, not all of the overall value at stake is going to be up for the grab. So, it is important to identify the correct ecosystem where you can play and win.

Second, implementation of an ecosystem strategy requires a firm performance across multiple dimensions, including technology, customer engagement, and culture. Hence, insurers should identify the critical capabilities that can act as a differentiating factor in the ecosystem and assess whether their organization has enough horsepower in the given areas.

Insurers in the Digital Ecosystem

To insurers, going from the viewpoint of an industry to an insurance ecosystems requires a significant shift in how they perceive their role in the economy. Currently, insurers have a limited and passive relationship with the clients. If insurers were to lose their distribution and consumer partnerships, their business models would be left with few choices. Adoption of an ecosystem perspective by reconsidering the traditional business model and partnerships, both outside and within the industry, could strengthen the insurer’s digital strategies.

Role of the new insurer

Insurers in a particular ecosystem may play multiple roles. The personal mobility ecosystem, for example, offers various opportunities to expand into areas such as vehicle purchase and maintenance management, traffic management, ride-sharing, carpooling, parking and vehicle connectivity. As a result, there are a number of opportunities for insurers to extend their positions.

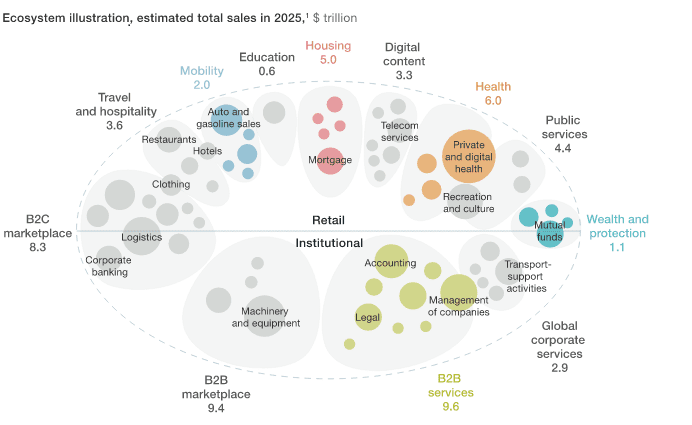

Replacement of New Insurance Ecosystems with many Traditional Industries by 2025

Importance of Partnerships

Since ecosystems enable and require a focus on risk reduction, relationship building will be a critical priority. For comparison, executives need to look no further than their recent efforts to collaborate with the Internet of Things (IoT) providers, which they adopted in an attempt to compensate for their vulnerability due to a lack of consumer touchpoints and dedication. In order to gather more fruitful alliances, insurers should adopt a similar mindset.

Challenges for insurer in an ecosystem

- Matching capabilities to ambitions

While many insurance firms are proactive in developing market-leading ecosystems, they are not always matched with their capabilities. When the attributes of companies doing exceptionally good at ecosystems are checked, less than 5% of the insurers were identified as ecosystem masters. This is the second-lowest of all the industries examined. There is no denying that insurers carry a lot to the table. The scope and variety of data they have are unparalleled. They have long-standing customer relationships that foster trust, and they have tremendous potential for frictionless business by partnering with the right players. The area where insurers fall short is having the right capabilities, technologies, and culture to fully exploit the ecosystem opportunity. - Don’t gamble on the right partner

Though insurers want a seat at the ecosystem table, it is essential for them to be careful about selecting who joins them there. The right partners allow an insurer to effectively collaborate and achieve economies of scale, skill, and scope –

Scale – Greater reach, cost advantage, and size are brought by the right insurance ecosystems partners. For example, a partner with scale may have enormous data that can be utilized to inform better customer experiences and insights.

Skill – Insurers will have access to a wide range of skills, technologies, and capabilities that they would not otherwise have had. This ranges from personalization and customization, machine learning, facial recognition, and digital marketing.

Scope – With the support of ecosystem partners, insurance companies can broaden their consumer value proposition, whose resources will increase their range of offerings and introduce new products. - Technological gap

The technological gap is one of the major challenges. In this technology-driven industry, insurers that are capable of and are prepared to integrate quickly with the modern distribution channels will be far more successful at achieving a set platform. Having any technological gap can lead to a lag in the business growth of an insurance firm as the market competition is increasing at a rapid rate. Hence, insurers will need to learn to run as fast as the digital platforms if they wish to keep up with this competition in the market. - Creating off-the-shelf products

Traditionally, insurers created off-the-shelf products and then sought customers that are willing to buy them. In this modernized era, customers are accustomed to personalized products that pay heed to their specific requirements at the time. Hence, insurers need to have a more modular approach that is based on generic products to gain an edge on the market competition. Moving beyond this product-focused model will demand both technological and organizational change in the insurance business.

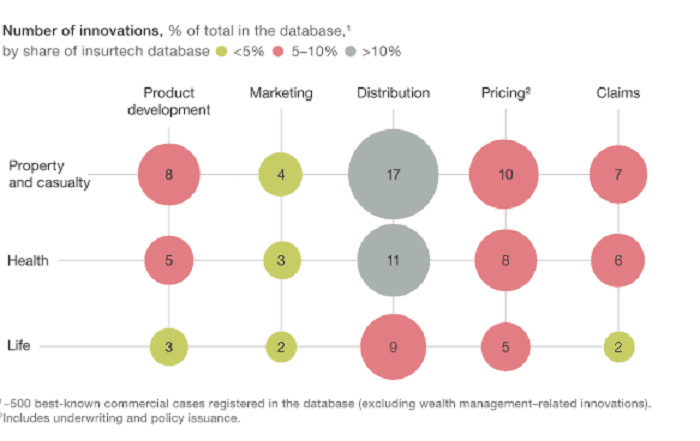

Insurtecs are focusing on Following Major part of the insurance industry

Image source: McKinsey

Opportunities for Insurance Ecosystems

By the implementation of digital ecosystems, insurance companies are betting big on opportunities having the potential to realign the global market.

One research by McKinsey shows that some companies have become clear market leaders with the help of digital technology. Still, at the same time, technology has reduced corporate earnings and overall value for many companies. By 2025, insurance ecosystems will drive 30% of global revenue.

Based on market capitalization, 7 out of the 10 largest companies are ecosystem leaders – Amazon, Alibaba, Apple, Alphabet, Tencent, Facebook, and Microsoft.

Putting customers at the heart of every digital activity has not only increased adoption but has also permitted companies to capture the previously unimagined.

As this revolution gains momentum, by 2025 McKinsey expects 12 distinctive and massive ecosystems to emerge around fundamental human and organizational needs. These 12 ecosystems will account for $60 trillion in revenues by 2025, or roughly 30 percent of all global revenues.

In this new digital world, while insurance is viewed as a risk-mitigation service for these 12 ecosystems, there is no reason for the insurance companies not to constitute their sub ecosystem that can address institutions and individuals.

Conclusion

Adaptation of insurance ecosystems and set platforms is essential for any insurance company to meet the requirements of the current digital market. Insurance businesses are now striving to achieve a more customized and personalized approach when it comes to client satisfaction and market competition.

{kind=link}